Rural families in developing countries face an increasing risk of losing their livelihoods to weather-related disasters. High-quality agricultural index insurance has proven to provide needed support in a disaster while also unlocking new investments for higher yields and incomes.

Alternative indexed financial instruments, including commitment savings accounts and contingent lines of credit, overcome some of the limitations of index insurance while providing similar benefits. A flexible blend of the three financial instruments can meet a rural family’s circumstances and need, strengthening their resilience across their journey to prosperity.

Highlights

- When small-scale farmers know there is a chance of losing crops to drought or other weather-related shocks, they tend to under-invest in productivity. While a shock itself can drive a rural family into poverty, the risk of a shock keeps them from achieving a better livelihood.

- Agricultural index insurance has been shown to provide needed support in the event of a shock as well as to unlock investments for greater productivity and income.

- New indexed financial tools, including a commitment savings account (CSA) and a contingent line of credit (CLOC) create an opportunity to blend indexed financial instruments to meet farmers’ circumstances and needs as a means to create a more resilient, prosperous future.

Rural families in developing countries do their best to manage a risk of losing their livelihoods to drought and other weather-related disasters. Instead of investing in improved inputs and other opportunities to increase their income, they often minimize risk as much as possible by avoiding more expensive productive inputs. They also keep savings in the form of livestock, granaries or cash under the mattress, each of which carries significant risk of loss.

The outcomes of these strategies depend on whether a farmer has a good or bad year. In a good year, a farmer harvests her crop and might sell any excess. She’ll pay off an agricultural loan if she has one. In a bad season, her harvest may fall far short of what her family needs. They will have to manage with less food and cash until next season’s harvest if she hasn’t sold the tools and assets needed to keep farming.

Today, indexed financial tools can help farming families avoid the worst impacts of a bad season. These tools may also unlock investments that improve incomes and livelihoods. When effectively blended, indexed financial tools can support farming families across their journey to a prosperous and resilient future.

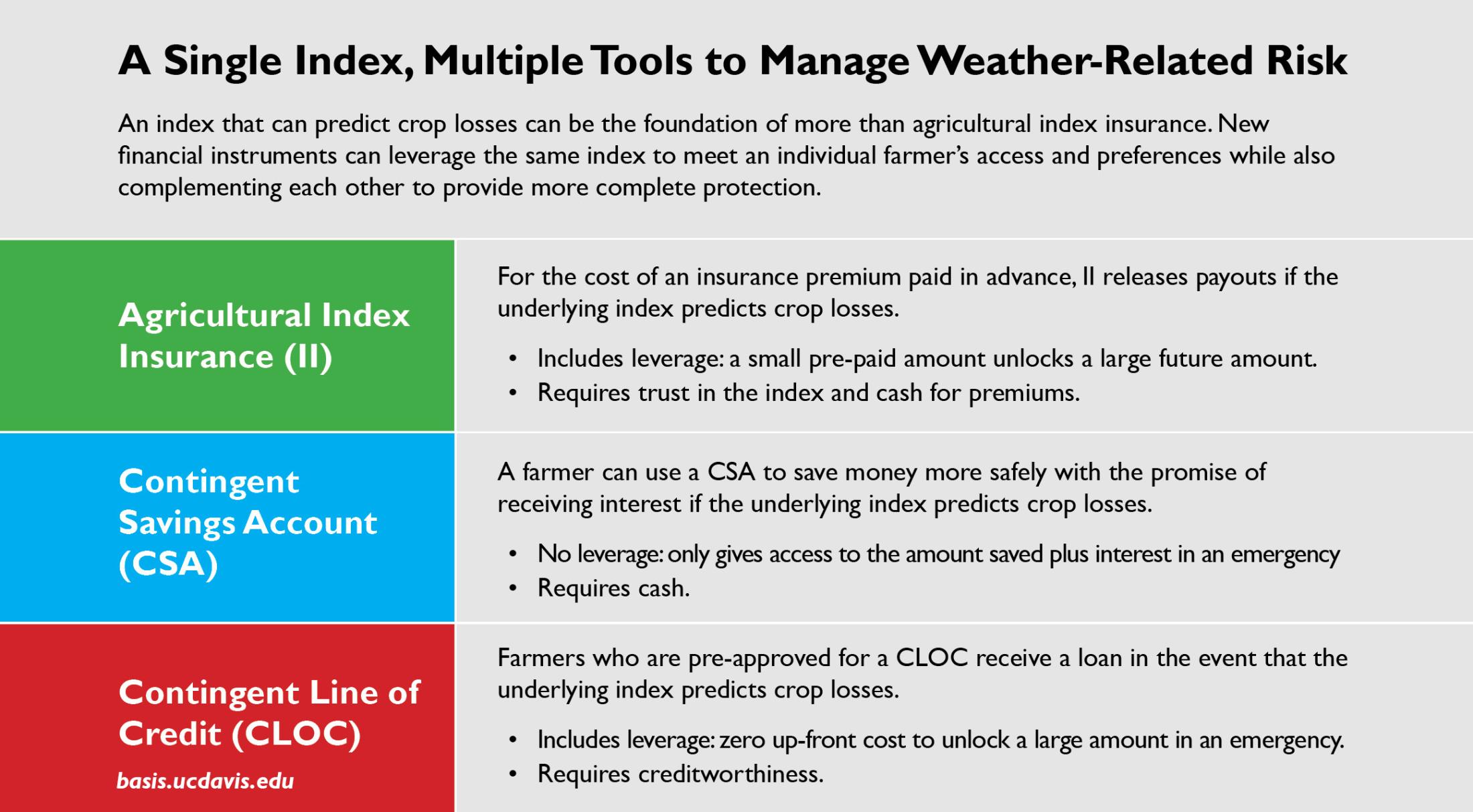

Farming with Index Insurance

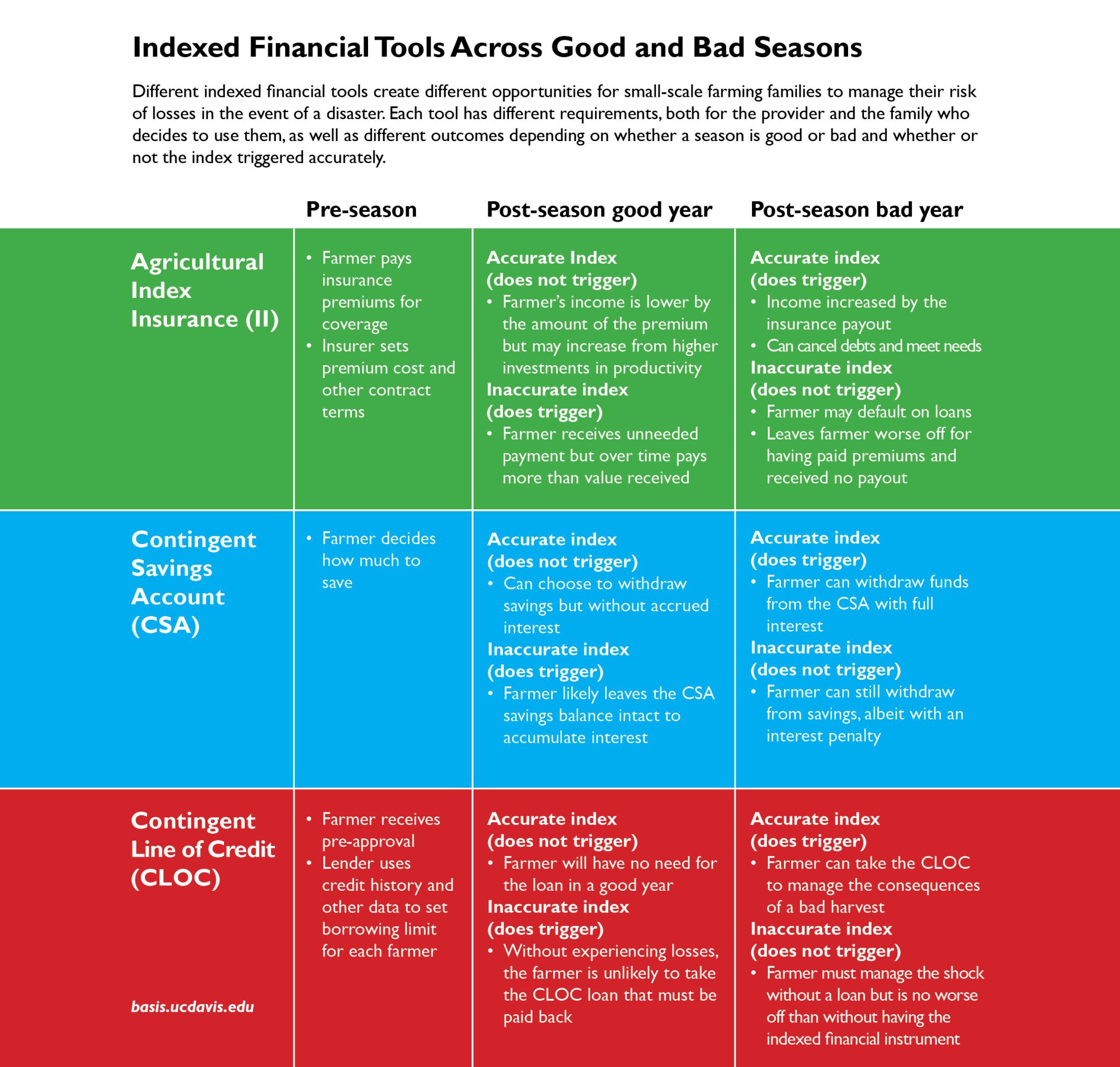

Index insurance is a low-cost form of insurance that bases payouts on factors that predict losses across a geographic area, such as satellite measurements of vegetation or estimates of average yields. High-quality index insurance provides security that farmers can keep farming after a bad year.

Field trials have shown that index insurance can also unlock investments in productivity. In Kenya, pastoralists who purchased Index-based Livestock Insurance (IBLI)[1] invested in veterinary care for the cows they had, increasing milk production worth an average of $5.95 per month. Index insurance for cotton farmers in Mali[2] increased planting by between 25-40 percent. We call this combination of protection in the event of a shock and investments in productivity “Resilience+.”[3]

With index insurance, a season with a good harvest can lead to two scenarios. In the first, the index insurance does not trigger a payout. The farmer sells her crop and cancels any agricultural loans. Her income will be less for having paid the insurance premium, but the protection may have unlocked her willingness to invest more for higher income. Alternatively, if the index insurance inaccurately triggers a payout, the farmer will have paid more over time than the value of the payout. In many index insurance products, the cost of false positives is already built into premiums, increasing the cost to farmers.

A bad harvest can also lead to two scenarios. If the insurance accurately releases a payout, an insured farmer receives needed funds in a time of crisis. However, if the index fails to release a payout, the insured farmer suffers the loss of her crop as well as the money she paid for insurance. Low-quality index insurance, which has a high risk of failing when farmers need funds the most, can leave people worse off for having purchased it.

Blended Indexed Financial Tools

In spite of the potential benefits of index insurance, sustained adoption has been a challenge. Index insurance is a complicated financial instrument that is hard to understand for households who have no experience with even conventional insurance. Index insurance policies are often expensive and payouts happen infrequently. Index insurance also comes with the risk that it won’t release payouts even if farmers experience a loss. There are other instruments that can leverage the same index to fill some of the gaps left by insurance.

A commitment savings account (CSA) is a type of savings account that only releases saved funds with full interest when its index predicts a bad season. Withdrawals can be made if the index does not trigger, but without full interest. A CSA is safer than informal savings and offers higher returns through interest, though its ability to manage risk is limited to a farmer’s own accumulated capital.

A contingent line of credit (CLOC) is a line of credit made available if the index indicates crop losses. Not all farmers can qualify for this loan. Like any other loan, it is made available based on credit history or income. Unlike insurance, which leverages today’s income for future payouts when they are needed, a CLOC leverages future income to manage financial need today. A field trial measured the impact of a CLOC in Bangladesh[4] and found that it increased productive investments that were similar to index insurance but without the up-front cost. In that study, the CLOC was restricted to long-time, well-trusted borrowers.

Offering these three instruments together opens up a number of possibilities beyond whether or not an index insurance contract releases payments accurately. In a good season when index insurance does not release payments, the scenario is the same as with insurance only. In the case of a false positive, when the insurance releases a payout even though there have been no losses, the scenario is also the same except that a farmer could choose whether or not to withdraw her CSA savings with accrued interest or to take a CLOC loan.

In a bad season, she has many more options. If the index correctly releases a payout, she not only has the funds from the insurance but can also decide whether to withdraw her CSA savings with interest or accept a CLOC loan. If the index fails and she receives no insurance payment, she can still withdraw from her CSA, albeit without the accrued interest. The CLOC will not disburse a loan, but she also hasn’t paid anything in advance to receive it.

Building Prosperity over Time

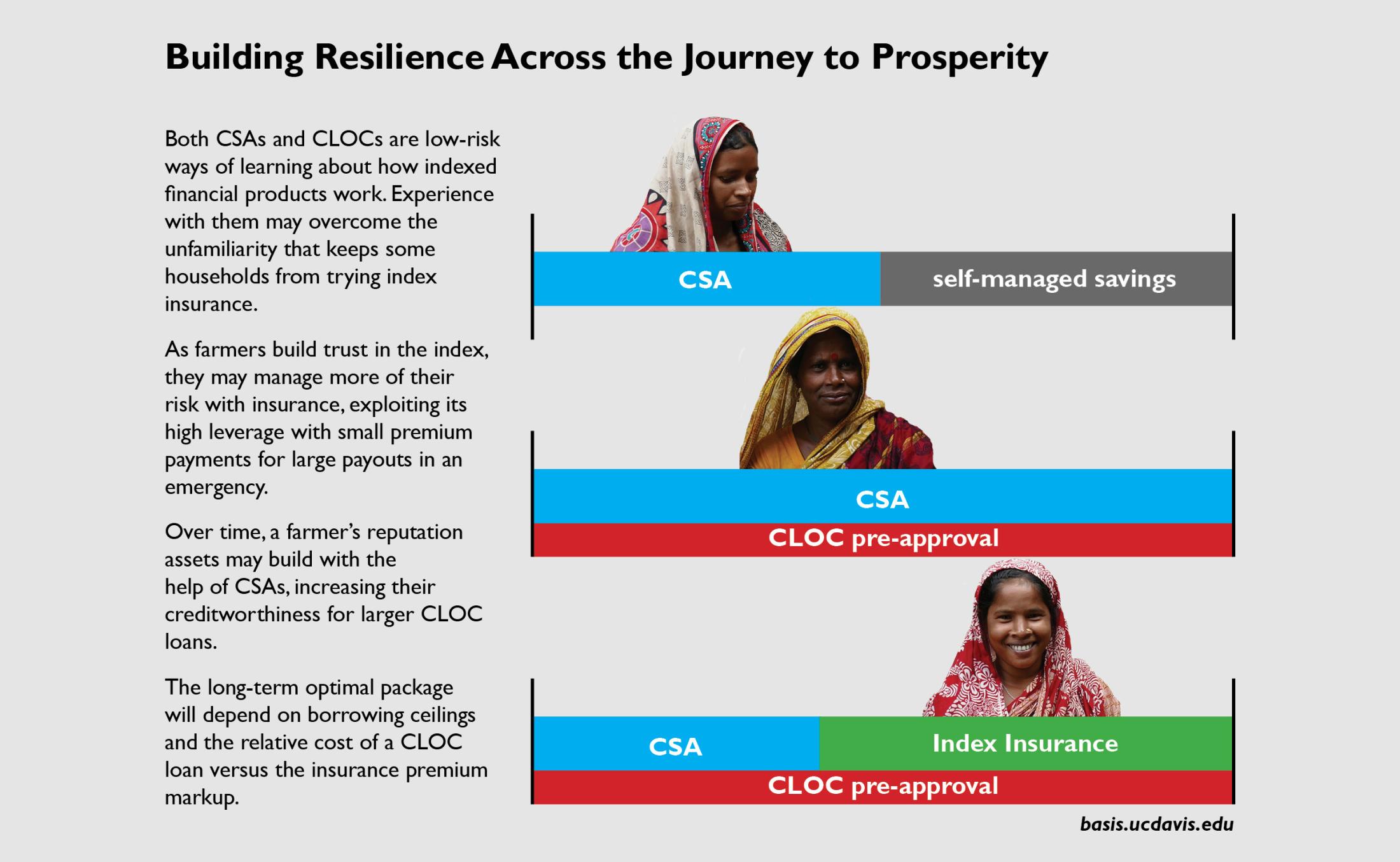

The blend of these three indexed financial instruments makes it possible for small-scale farmers to dynamically manage their risk over time. CSAs and CLOCs are also low-risk ways to learn about how indexed financial products work.

As farmers build up experience and trust in the index, they may shift from a CSA or CLOC to managing more of their risk with insurance because the small amount paid in premiums provide substantial payouts in a bad year. As a farmer’s reputational assets build up, they may also have access to larger CLOC loans.

The optimal mix of these instruments for any individual farmer can change over time. Blending these tools effectively expands the means to manage risk from year to year, positioning farmers to unlock a more prosperous and resilient future.

[1] Jensen,N.D., et al. 2016. “Index Insurance Quality and Basis Risk: Evidence from Northern Kenya.” American Journal of Agricultural Economics.

[2] Stoeffler, Q., et al. 2022. “The Spillover Impact of Index Insurance on Agricultural Investment by Cotton Farmers in Burkina Faso.” World Bank Economic Review.

[3] Carter, M. 2021. “Generating Resilience+ to Reduce Poverty and Spur Agricultural Growth.” MRR Innovation Lab Evidence Insight.

[4] Lane, G. 2022. “A New Type of Indexed Loan to Address Risk and Build Beyond Resilience.” MRR Innovation Lab Evidence Insight.

This report is made possible by the generous support of the American people through the United States Agency for International Development (USAID) cooperative agreement 7200AA19LE00004. The contents are the responsibility of the Feed the Future Innovation Lab for Markets, Risk and Resilience and do not necessarily reflect the views of USAID or the United States Government.